Industry data supports the shift. In a study by Big ‘I’ and Reagan Consulting, it showed that top-performing companies are not focusing on costly expansion. Instead, they are increasing client retention, improving revenue per employee, expanding account rounding, and reducing administrative inefficiencies. In 2025, top-performing agencies generated $228,321 in revenue per employee. It clearly shows that operational efficiency is one of the strongest indicators of profitability.

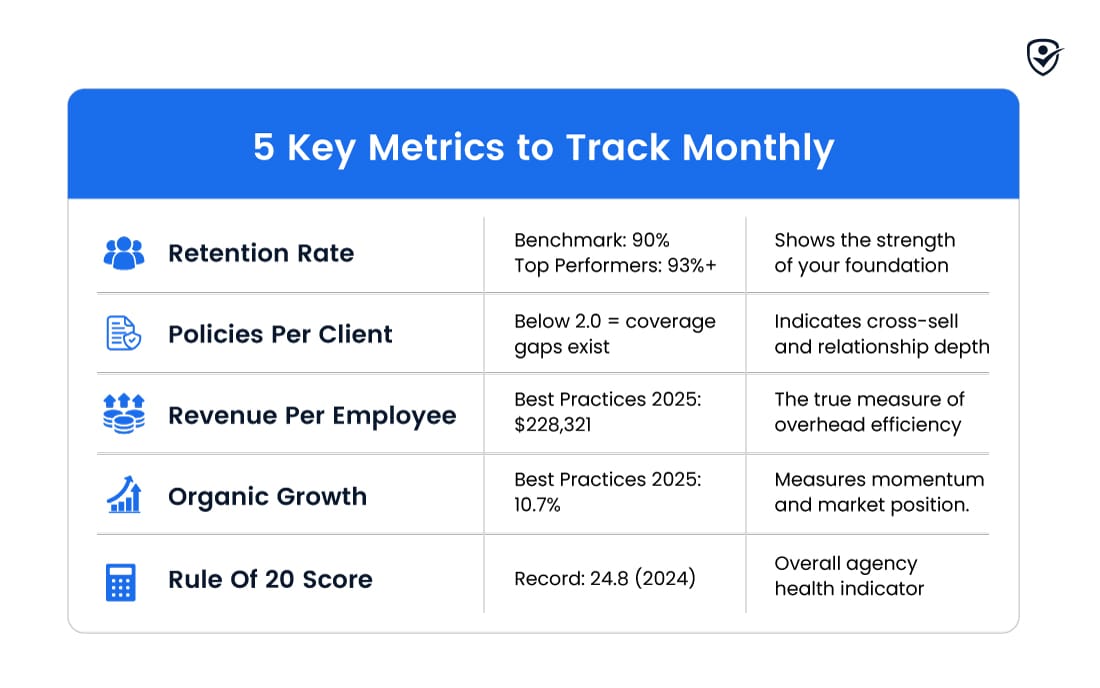

Another way insurance agencies measure their growth is through the Rule of 20. Add your agency’s organic growth rate to half your EBITDA profit margin. A score of 20 or above indicates a healthy, scalable agency. For example, an agency with 10% organic growth and a 20% EBITDA margin scores exactly 20 (10+ half of 20). Most agencies below this threshold are growing revenue but losing profitability to overhead costs.

This guide explores five practical insurance agency growth strategies without increasing overhead expenses.

Top Insurance Agency Growth Strategies without Overhead

The following strategies help insurance agencies focus on practical, operational changes to grow revenue and scale efficiently without adding overhead costs.

Maximize retention before pursuing new clients

Retention is a major factor that separates agencies that grow profitably from those that grow expensively. According to Big ‘I’ and Reagan Consulting, top agencies maintain a 90% to 93% retention. Even a 2% to 3% improvement in retention means tens of thousands of dollars preserved, almost $120,000, for a mid-size agency.

With more people comparing insurance prices and changing companies through 2025, renewals have become the most important sales opportunity.

Three top tactics lift retention without adding any headcount:

Run proactive renewal outreach 60–90 days before the renewal date

Start contacting clients every 60-90 days before renewal, instead of waiting for the last moment. Renewal outreach at this stage typically involves three touchpoints: an initial coverage review call, a documentation request follow-up, and a final confirmation email before the renewal date. Structuring these in your AMS as automated tasks ensures no renewal falls through the cracks.

Review the carrier policy form changes at every renewal

Make sure you check and record any changes in renewal. Because insurance companies often change their policy wording and may limit their coverage.

When you review policies carefully, you help clients avoid surprises such as finding that anything covered in their insurance is no longer part of the policy.

Build referral partnerships that replace paid advertising

Referral partnerships help you get leads without investing in paid ads. For this purpose, you can work with people like HRs, real estate agents, and mortgage brokers who already have a network and can easily refer you. Referral partnerships easily replace paid acquisition with trust-based lead flow.

Three referral partnership structures that work without overhead:

Build strategic professional alliances with non-competing service providers

Work with some professionals who serve the same type of clients but do not compete with you. For example, commercial insurance agencies can partner with real estate brokers and payroll companies.

On the other hand, if you are running a personal insurance agency, you can work with mortgage brokers, financial planners, and estate lawyers. Building partnerships and referrals is crucial too.

Align with carriers growing in specific segments for inbound referrals

You can also make carrier network referrals. Partner with insurance companies that are working in your niche. Because they often send clients to trusted agencies that are strong in the area.

Build a structured client referral ask into your post-claim and post-renewal workflow

Client referral programs help you get new business from happy customers. Long-term clients are the best people to refer others to because they trust you.

If you ask for referrals after a claim is successfully handled or a renewal is completed, satisfied clients are more likely to recommend you to others. This brings in new clients without spending any money.

Niche specialization: compete on expertise, not price

Trying to serve everyone may seem like an agency is busy, but it’s not profitable. When you focus on one area only, you don’t compete on price anymore. You start competing in what you know, which makes it harder for others to compete.

Choose one niche based on existing book concentration, not aspiration

The easiest niche to grow is the one you already have. Check your AMS system and sort clients by industry. You’ll usually see one or two industries where you already have several clients. Start there because you already know the market, have experience with claims, and can use existing client references.

Build expertise in the coverage gaps your niche clients are underinsured for

Learn what your niche clients are missing in their insurance coverage. Many small and medium businesses still don’t have enough protection, especially in cyber insurance and employment practices liability.

If your agency becomes good at offering these for a specific industry like construction, retail, or professional services, you can become a trusted insurance provider.

Use niche expertise to command better carrier terms, not just better marketing

Niche Specialization helps leverage with carriers, leading to better pricing, faster underwriting decisions, and preferred appointments. When you are a niche expert and send more business to insurance companies, they start trusting you, offer more competitive pricing, and prioritise your quote requests.

It’s best to keep carrier networks and relationships. Attend carrier advisory councils, respond to updates, and maintain production volume with top 3-5 carriers. Agencies with preferred status receive first-look referrals and appointment invitations in growing segments.

Producer development: grow revenue before growing headcount

For agency growth, it is essential to enhance the productivity skills of your existing producers. Because when you hire a new producer, you have to invest in them (onboarding, salary, tools) before they generate revenue.

Increase output from existing producers before adding new ones

Increasing output with the help of your existing producers. Do not rush to hire new producers. Check where the issue is, if they are not productive. The issue is not with the people, but often, producer capacity is underutilized due to a lack of visibility and support.

Make producer metrics visible weekly, not quarterly

When producers have proper checks and balances on their sales teams every week, sales work improves. Sales workers can perform better when they are aware of their numbers weekly. They can know the number of clients they have, how often they sell extra products, and how many clients they are working on.

When you do recruit, invest at the NUPP benchmark, not above it

Healthy agencies keep producer payroll around 1.5% to 2% of total revenue. This is called a safe range for growth.

If you spend more than this, you are adding more costs even before the new producer starts bringing revenue for your agency. So, be careful while you hire new staff because hiring too many people can cost you more and disrupt your revenue cycle.

Delegation without headcount: the operational lever most agencies skip

Producer time is important, so every hour a producer spends on administrative tasks is an hour that is not spent on talking to clients, handling renewals, and finding new business.

Identify the administrative tasks consuming licensed producer time

COI processing, policy checking, renewal follow-ups, claim status updates, carrier emails, and AMS data entry are time-consuming tasks.

There is no need for a licensed producer to perform these tasks. They take time away from client meetings and new sales calls. Once you identify the time-consuming tasks, delegate those tasks to any virtual or onsite insurance assistant.

Use a trained insurance VA to scale throughput without adding salary overhead

A virtual assistant for insurance agents trained in insurance tasks like COI handling, AMS updates, renewal scheduling, and carrier portals can handle routine admin work. The shifting of administrative workload away from licensed staff increases selling capacity without adding a full-time in-house payroll.

Measure the result in revenue per employee, not hours saved

The real sign that delegation is working is higher output per person, not fewer hours worked.

Top agencies generate $228,321 revenue per employee. If your agency is around $150,000, you need to remove administrative work from producers and delegate it to support staff to help producers reach this revenue count.

How to Use 2026 Market Conditions to Your Agency’s Advantage

Every growth strategy works when market conditions support your agency. In 2026, agencies that focus on retention, cross-selling, and client relationships have more opportunities to grow without increasing overhead.

Use the carrier profit recovery to place harder risks

The US property and casualty insurance saw a major increase in underwriting profitability during 1st nine months of 2025, where net underwriting gains reached nearly $35 billion. Because insurance companies are earning more money again, they are willing to have new clients and offer coverage in an easier way than before.

This is also a good time for you to connect with old clients who left due to high prices and limited coverage. Get your clients back before the market becomes strict again.

Target the shopping surge in personal lines

After easy insurance policies, people are exploring new cars, homes, and rental insurance. So, it’s a good opportunity for insurance agencies to pitch their clients and ensure they get better deals.

Provide market-competitive rates to clients to grab their attention. Get the benefit from this opportunity as much as you can because once prices get stable, fewer people will switch their insurance providers.

Evaluate acquisition targets

Interest rates have gone down, so borrowing costs are low. This is a good option for you if you want to grow by buying another agency. Contact the small agency owners who are willing to sell their agencies. Buying an existing $500,000 client portfolio often costs you less than starting from scratch.

It saves the agency’s time, which would have been spent talking to clients one by one to get existing client payments.

Metrics That Indicate Healthy Insurance Agency Growth

An agency that is growing but is unable to track its retention, policies per client, or revenue per employee is not actually managing the growth. They are growing, but without clear directions.

Retention rate: the metric that shows whether your foundation is solid

The industry benchmark is 90% retention. Top-performing agencies achieve 93% or higher. If you are below 90%, you are spending money to replace clients you are losing instead of growing.

Policies per client: your cross-sell health indicator

Policies per client are your cross-sell health indicator. Industry average sits around 2.1 policies per client. High-performing independent agencies push this to 2.8–3.2 through structured account rounding at renewal.

If it is above 3, it means clients trust you more and keep most of their insurance with your agency.

Revenue per employee: the overhead efficiency benchmark

If the revenue per employee is high, it means the agency is in a growth phase. But if the revenue is growing, but the profit per employee remains low, it means you are hiring more people, increasing admin tasks, but the revenue is the same. In this way, the business looks bigger, but profit doesn’t improve much.

Conclusion: Scaling an Agency Without Overhead Cost

The major factor that separates high-growth agencies from busy ones is not budget or headcount; it is extracting more value from existing staff. They retain clients for a longer span of time, deepen their existing relationships through cross-selling, and build referral networks. This approach replaces paid leads and protects producer time by delegating admin work to trained support staff.

Many insurance agencies delegate their time-consuming tasks, such as COI processing, renewal reminders, and AMS data updates, to a virtual insurance assistant. It allows producers to focus on selling and building client relations and managing their clients.

So, stop confusing busyness with growth, and unlock your producers’ potential by letting a trained professional handle the paperwork.