The accounts receivable process is how a business makes sure it actually gets paid for what it sells. It covers everything from agreeing on credit terms with a customer to collecting and recording their payment. When this process works well, cash flow stays predictable. When it doesn’t, finance teams spend more time chasing money than managing it.

In this guide, you’ll find the full accounts receivable processing cycle broken down into seven steps, the five KPIs worth tracking, the most common bottlenecks that push DSO higher, and practical ways to improve your results.

What is the Accounts Receivable Process

The accounts receivable process is the structured, end-to-end cycle a business follows to convert outstanding invoices into collected cash, the moment credit terms are agreed to the moment payment is posted and reconciled.

AR is the part where completed sales actually turn into money in the bank. One thing to remember is that an unpaid invoice is not income. It’s a promise to pay the outstanding amount. The accounts receivable cycle closes that gap as quickly as possible.

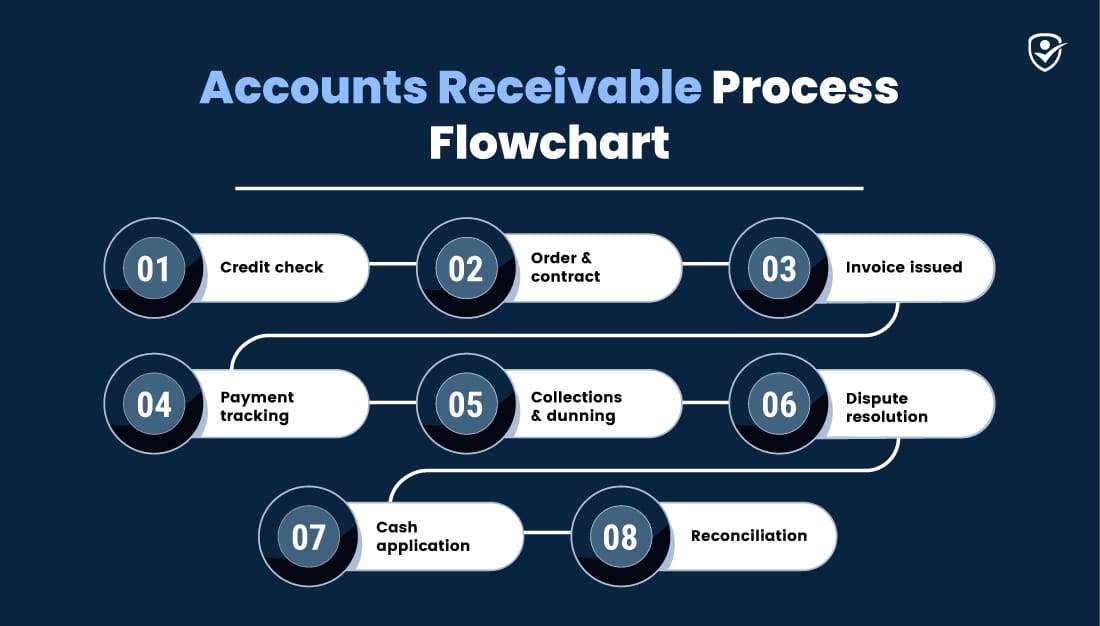

Accounts Receivable Process Flow: The 7 Core Steps

The accounts receivable process has a clear sequence where it identifies a problem at any stage and delays everything that comes after it. Understanding each step of this accounts receivable workflow helps finance teams identify where exactly cash collection slows and fix it at the source.

Here is the what the accounts receivable process flowchart looks like:

Credit check→Order & contract→Invoice issued→Payment tracking→Collections & dunning→Dispute resolution→Cash application→Reconciliation

This is important to understand every step for businesses so they can know at what step cash collected gets affected. The steps in the accounts receivable process follow a clear sequence, and a problem in one step delays the process of the next step.

Step 1: Credit evaluation and approval

Before extending payment terms, companies review whether a customer can actually pay. This process of reviewing credit scores, trade references, and payment history is known as credit management.

Based on the review, business sets a credit limit i.e. the maximum amount a customer can owe at the given time. Payment terms, such as net 30 or net 60, are defined at this stage.

This stage is crucial as bad credit decisions can easily become the root cause of bad debt write-offs. Business won’t be able to recover money from a customer who cannot or won’t pay. The entire accounts receivable process starts here.

Step 2: Sales order and contract setup

Once the credit approved on the agreed-upon-good or services are documented in a sales order or contract. The record contains details of what is being sold, the quantity, price, delivery details, and payment terms.

Based on this document invoice is generated. If the sales order mismatches with the invoice, like a wrong price or incorrect quantity, it will likely create a dispute and delay in payment.

Therefore, it is crucial to set up billing at this stage to prevent problems downstream. A transparent sales order means a clean invoice and faster payment.

Step 3: Invoice generation and delivery

When a sales order is confirmed, the business generates and sends an invoice to the customer.

The invoice must include two things:

- Invoice number

- Itemized products or services

- Payment terms

- Due date

- Accepted payment methods

- Accurate business details

Any missing or incorrect information can lead to invoice rejection.invoice delivery speed matters for finance teams. So, if your payment terms are net 30 but you send the invoice three days after delivery, you’re operating on net 33. The gap directly increases days sales outstanding (DSO).

That’s why businesses switch to e-invoicing through ERP systems to eliminate email or postal lag. This way invoices are instantly generated and the due date clock starts right at the moment.

Step 4: Payment tracking and dunning

Dunning is a structured, escalating reminder process designed to collect payments before and after they become overdue. A documented dunning schedule removes guesswork and keeps follow-up consistent. A typical collections policy looks like this:

- 7 days before due date (friendly payment reminder)

- On the due date (payment confirmation follow-up)

- 7 days overdue (formal overdue notice)

- 30 days overdue (escalation to collections)

Ad-hoc, inconsistent follow-up is the single most common reason invoices remain unpaid. When reminders depend on individual judgment rather than a documented collections policy, accounts slip through the cracks and invoices age into the 60–90 day overdue bucket.

Tracking this against your AR aging report shows exactly which accounts need immediate attention.

Step 5: Dispute and deduction management

When a customer disputes an invoice, payment is usually delayed until the issue is resolved. Common reasons include pricing differences, billing mistakes, quantity issues, damaged goods, or unexplained short payments.

Unresolved disputes are one of the top drivers of high DSO, not because the customer refuses to pay, but because the invoice sits open in someone’s inbox while the dispute waits for attention.

Every day it stays unresolved is a day added to your collection cycle.

In industries like CPG and manufacturing, deductions management is a specific sub-process within AR. Customers regularly deduct amounts for promotions, returns, or delivery shortfalls. Each deduction needs to be reviewed, validated, and resolved individually before the invoice can be closed.

Step 6: Cash application and payment matching

Cash application is the process of matching incoming payments to the correct open invoices and posting them to the general ledger. It is the step where money received in the bank becomes revenue recognized in the books.

Problems happen when customers pay partial amounts, combine multiple invoices into one payment, or omit remittance details entirely. Without clear remittance processing information, the AR team has to manually investigate each payment.

This creates unapplied cash; money sitting in the bank that hasn’t been matched to an open invoice. Unapplied cash is a hidden working capital problem that most finance teams underestimate. It overstates outstanding AR, distorts aging reports, and makes cash forecasting unreliable.

For businesses processing high volumes of B2B payments or lockbox processing, automated cash application tools significantly reduce matching errors and free up AR staff for higher value work.

Step 7: Reconciliation and AR reporting

Reconciliation is the final step in the accounts receivable process cycle. It verifies that all payments received match both the AR subledger and the general ledger, confirming that what the system shows as collected actually reflects what the bank received.

The reports generated at this stage feed directly into management reporting, tracking DSO, aging buckets, bad debt ratios, and overall AR performance. These numbers tell finance leaders where the process is working and where it is breaking down.

Accurate reconciliation is also a prerequisite for a reliable financial close. Without it, reported revenue and outstanding balances cannot be trusted.

How to Measure AR Process Performance: Key Metrics

You cannot improve what you do not measure. These 5 KPIs give a complete picture of the accounts receivable management process. They include how fast you collect cash, how well your process works, and the level of credit risk you carry.

Days Sales Outstanding (DSO)

What it measures: It measures the average time to collect payment after an invoice is issued.

Formula: DSO = (Accounts Receivable ÷ Total Credit Sales) × Number of Days

Example: AR balance = $500,000. Total credit sales over the past 90 days = $1,800,000.

DSO = (500,000 ÷ 1,800,000) × 90 = 25 days

Every extra day of DSO is a day your cash is sitting with a customer instead of in your bank. For a business with $2M in monthly credit sales, a DSO of 45 days instead of 30 means roughly $1M in additional working capital tied up in unpaid invoices. Industry benchmark: B2B average DSO is 35–45 days. Top-quartile performers achieve sub-30 days.

Collection Effectiveness Index (CEI)

What it measures: It measures the percentage of receivables collected as cash during a specific period.

Formula: [(Beginning AR + Credit Sales − Ending Total AR) ÷ (Beginning AR + Credit Sales − Ending Current AR)]

Example:

- Beginning AR = $400,000

- Credit sales = $600,000

- Ending total AR = $300,000

- Ending current AR = $150,000

- CEI = [(400,000 + 600,000 − 300,000) ÷ (400,000 + 600,000 − 150,000)] × 100 = 82%

This means the team collected 82% of everything it was realistically able to collect in that period. A CEI below 80% signals that a significant portion of collectible AR is being left unpursued. A declining CEI is an early warning sign before DSO starts to climb.

AR Turnover Ratio

What it measures: How many times a business collects its receivables in a year.

Formula: AR Turnover = Net Credit Sales ÷ Average Accounts Receivable

Example: $6,000,000 ÷ $500,000 = 12×

A ratio of 12 means your business collects its entire receivables balance roughly every 30 days. A lower ratio, say 6, means it takes 60 days on average, which doubles the working capital tied up in AR and increases exposure to bad debt.

Bad Debt Ratio

What it measures: It measures the percentage of receivables that could not be collected and had to be written off.

Formula: Bad Debt Ratio = (Bad Debt Write-offs ÷ Total Credit Sales) × 100

Example:

($50,000 ÷ $2,000,000) × 100 = 2.5%

A bad debt ratio of 2.5% on $2M in annual credit sales means $50,000 written off as uncollectable every year. Most of this traces back to Step 1, poor credit decisions at the start of the accounts receivable process. Tracking this ratio over time shows whether your credit management standards are tightening or slipping.

Percentage of invoices disputed

What it measures: The percentage of invoices that become disputed during a billing period.

Formula: Invoice Dispute Rate = (Disputed Invoices ÷ Total Invoices Issued) × 100

Example: (30 ÷ 1,200) × 100 = 2.5%

A dispute rate of 2.5% sounds small but on 1,200 invoices that is 30 open disputes at any given time. Each one stalling payment until resolved. More importantly, a rising dispute rate is a leading indicator of upstream problems: errors in Step 2 or Step 3 that are showing up as disputes in Step 5. Fix the dispute rate and DSO follows.

Common Bottlenecks in the Accounts Receivable Process

Most of the inefficiencies in AR come through 5 areas. Every area creates effects on cash flow, increasing delays and adding operational pressure.

1. Late or inaccurate invoice delivery

Late invoices cause payment delays. If invoices are sent several days after goods or services are delivered, the actual payment period becomes longer than agreed.

For example, a business with net 30 terms and a 4-day invoicing delay is effectively operating on net 34. On $6M in monthly credit sales, this can leave around $800,000 tied up in working capital. Sending accurate invoices on the same day helps reduce delays and improve cash flow.

2. No standardized dunning process

When payment follow-up depends on individual judgment rather than a documented process, invoices slip through the cracks.

Research shows that invoices reaching 90+ days overdue have a recovery rate below 40%. It means more than half of that debt will likely never be collected.

A standardized dunning cadence keeps every invoice on a consistent follow-up schedule. It removes the risk of accounts being forgotten. Without it, late payment becomes a pattern customers learn they can repeat.

3. Manual cash application errors

Manual cash application across high volumes of invoices produces error rates that compound quickly. When payments are mismatched or left unapplied, AR balances appear higher than they actually are. They overstate outstanding receivables by as much as 5–10% in businesses processing hundreds of payments monthly.

This distorts DSO figures, triggers unnecessary collection calls on already-paid invoices, and creates reconciliation headaches at financial close.

4. Unresolved disputes without an SLA

Every unresolved dispute is an invoice that cannot be collected. Without a defined SLA, disputes sit in inboxes for weeks, sometimes months.

A single disputed invoice worth $50,000 sitting unresolved for 45 days represents 45 days of DSO drag on that amount alone. Across a portfolio of disputes, this effect compounds fast.

Businesses without a dispute resolution SLA consistently carry 15–20% more aged debt than those with one.

5. Limited real-time visibility into AR aging

Teams that rely on old AR reports may focus on the wrong accounts. They could spend time following up with customers who have already paid while missing overdue invoices that need attention.

Real-time AR visibility helps teams prioritize the right accounts and collect payments more efficiently. When AR teams do not follow a proper routine, issues like unpaid disputes and manual payment matches start piling up.

AR teams can also perform well by setting specific time for resolving disputes and grouping payment follow-ups together.

How to Improve Your Accounts Receivable Process

Improvement in accounts receivable happens in two stages: 1) Quick improvements that can be made immediately without new technology. 2) Long-term changes that take time but deliver lasting results.

Quick wins: improvements you can implement now

These four improvements require no new technology or budget. You can start them today:

Standardize your invoice format

Use one standard template for billing instead of using different ones. Add correct business details, payment instructions, due date, and a clear layout to it. It helps in reducing invoice errors and prevents delays caused by them.

Create a clear payment follow-up schedule

Set a documented process for reminders and collections. Invoice sent on day 1, reminder on day 7, overdue notice on day 14, and escalation on day 30.

AR teams that block specific time for dispute resolution and batch their collection follow-ups, much like how financial advisors structure their work, process more accounts in less time. Consistency in follow-ups directly reduces the number of days invoices spend in the overdue bucket.

Adjust credit terms for slow-paying customers

Review which customers pay late on a regular basis. After identifying them, consider lowering their credit limit, shortening payment terms, or asking for payment upfront.

Send invoices immediately

Send invoices on the same day as the delivery of goods or services. The faster you send invoices, the higher the chances of receiving payment sooner.

Strategic improvements for long-term AR efficiency

Below are four strategic improvements that deliver lasting results for your accounts receivable process.

Automate cash application and payment follow-ups

Use AR automation to match payments automatically and send schedule reminders. This can reduce collection time and improve cash flow. It works even better when connected with a well-organized ERP system.

Add a self-service payment portal

Allow customers to view invoices, download statements, and make payments online. This makes paying easier, reduces questions to the AR team, and creates a clear record of customer activity.

Segment customers by payment behavior

Not all customers pay the same way. So, group customers on the basis of patterns such as reliable payments, frequent delays, or repeated disputes. After grouping them, use different approaches for each group to improve efficiency.

Build real-time AR dashboards

Replace static reports with live dashboards that show overdue invoices, payment status, disputes, and aging balances. Real-time visibility helps teams focus on the right accounts and act faster.

Where Accounts Receivable Fits in the Order-to-Cash Cycle

Accounts receivable is the backbone of the order-to-cash (O2C) cycle. It covers everything from receiving a customer order to delivering the product or services, sending an invoice, collecting payment, and recording the revenue.

You can call AR a stage where completed sales are turned into actual cash for businesses. But keep in mind that improving only AR is not enough. If there are errors in sales orders, AR teams will spend more time handling disputes.

Similarly, if payment and reporting systems are not connected, there are chances of inaccuracy in cash forecasting.

So, O2C performance depends on all connected processes working well together, not just AR.

Conclusion: Build a Faster and Stronger AR Process

The accounts receivable process plays a key role in turning credit sales into cash. Poor AR management can cost businesses 4-5% annual revenue. Companies can reduce delays and cash flow by following the seven key steps and KPIs like DSO and CEI.

Quick improvements like standardizing invoices and setting a clear follow-up schedule can deliver immediate results. Automation and real-time reporting can improve efficiency on a large scale.

If your team is stretched across collections, dispute resolution, and cash application simultaneously, a dedicated accounts receivable virtual assistant can take the manual workload off your plate, so your finance team focuses on decisions, not data entry.

Start with one quick win this week. Pick the step where your process is weakest and fix that first.